Most eyes and attention were on the federal treasurer on 3rd May as the budget was brought down. But being the first Tuesday of the month, the Board of the Reserve Bank of Australia also met. After many months of leaving official interest rates steady, they made the decision to cut them this month. What does that mean for you?

The majority of people don’t worry about interest rates other than how it impacts on them. Many people don’t really give much thought to the rise and fall of interest rates and the reasons behind them.

But the world’s central bankers usually only cut interest rates when they think their economies need a boost. In other words, when a country’s economy is tanking, a central bank may cut interest rates to try and stimulate demand.

The thinking behind this is that if credit is cheaper, people might be more inclined to borrow. Preferably, they’d like them to borrow a larger amount than they might otherwise have borrowed if interest rates were higher. Our economies are not growing if debt is not increasing.

But because lower interest rates are associated with lower economic growth, this also has the effect of lowering confidence in the markets and the economy, even if it is at a subconscious level. It is worth remembering that we are now well below the so called “emergency” interest rate level we were at during the GFC. This means that lowering rates is likely to have the opposite effect than was intended by the Reserve Bank. All that negative interest rates do is confirm that our economies are in grave trouble and reduce overall confidence in our economies.

In addition lower interest rates are not good news for those who save or people who rely on income from cash deposits, whose incomes have just dropped yet again. Ironically, while low interest rates benefit those who already have mortgages and other loans, it hurts those who are actually saving for a home or other big ticket item, thus keeping them from borrowing sooner than they might with higher interest rates. It also means that people who rely on interest for income have less to spend, thus contributing less into the economy.

There is also the law of diminishing returns, in that each subsequent interest rate cut has less effect and the impact of the cut has a shorter actual duration. So any possible benefits this cut might have had will last a shorter time and be less effective than the last round of rate cuts, until they lose all effectiveness.

It brings to mind Einstein’s definition of insanity. Doing the same thing over and over and expecting a different result. This cut will not be any different. If the last dozen or so cuts that we have had have not had the required result of stimulating the economy, why will this one be any different?

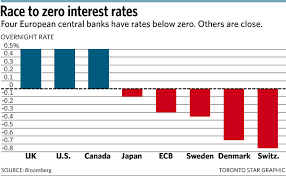

Japan, Sweden and Switzerland currently have a negative interest rate policy (NIRP) and countries like Europe and until recently, the US have zero interest rate policies, based on this very assumption that it will stimulate the economy and increase demand.

It’s not working. For example, in Japan, more people are saving and hoarding cash the lower interest rates go, especially when they go into negative territory. If these zero or negative interest rate policies were effective at all, these countries would have booming economies. They don’t.

The world is already awash with debt. Trying to solve a debt problem with more debt by lowering interest rates will not work, particularly when a lot of that debt is tied up in non-productive assets that do nothing to make a real contribution to the economy.

Given the sluggish nature of global economies and the uncertainty of our own, now might not be the time to be getting further into debt, as attractive as the low interest rates might be.

Here are some things to consider in a low interest rate environment:

- Pay off debts: Instead of racking up more debt, use the low interest to pay off debts instead.

- Look for better rates for debts: Use the low interest rate as an opportunity to negotiate a lower rate on the debts you do have. Home loans are a good place to start, but also look at other loans and credit cards. Maybe consolidating them all into one low interest rate loan can help.

- Start saving or boost existing savings: If you have low or no debt, think about channeling more money into savings. This can then be directed into investments.

- Search for yield: Lower interest rates mean it can be a struggle to obtain a reasonable interest rate on your savings, but there are tools available to help you find those higher interest bearing accounts. Websites such as Canstar, Finder and others, for example, can help you search for and compare various bank accounts for higher interest rates. Be aware though that these websites may not list all banks or accounts available and always read the terms and conditions. These sites can also be useful for finding low interest rates for loans as well.

- Take advantage of low interest rates if necessary: Conversely, while it might not actually be the best time to take on more debt, if your car or a big ticket item is long overdue for replacement, there might be no better time to use low interest to your advantage. However, try to make extra payments to pay this off as soon as possible, rather than just make the minimum repayments.

Lower interest rates might make it tempting to borrow more money than you normally would, or get further into debt, but warned this may be a trap. It can be easy to become overextended should interest rates rise.

It is unlikely that official interest rates will rise soon, but that doesn’t mean that the banks won’t raise interest rates outside of the official interest rate. Banks obtain a percentage of their loan funds from overseas and are reliant on Australia maintaining its AAA credit rating and confidence in Australia’s economy. Banks are also reliant on depositor’s money to provide the balance of their loan funds. They are unlikely to attract too many depositors if interest rates are too low.

But most importantly, think about why interest rates are being lowered by the RBA. It’s a sign the economy might not be doing as well as many people suppose. Some businesses might not be financially sound due to slower economic conditions and the threat of closure is ever present. If your job is your only source of income, how well could you pay back your loans if you lost your job?

![]()

Great article, exactly what I needed.|

This website is amazing. I will recommend it to my son and anybody that could be interested in this subject. Great work guys!