We, as Australians, seem to have developed a love affair with property over the past 40 plus years. Property has became an investment class rather than just a provider of shelter and the consumable item that it should be. A place to park wealth rather than used to create it. This continuously raises the possibility of a bubble.

There has been a lot said, many megabytes devoted to and much news ink used in commentary about a bubble in Australian housing.

People ask me if I think that Australian housing is in a bubble. I usually answer in the affirmative saying it’s looking very frothy and furthermore tell them that Australia’s and many of the world’s housing has existed in a bubble for the past 45 or so years.

I will get back to this in a moment, but first I’d like to say that just because Australian housing is in a bubble, does not mean that it cannot continue for a while longer, although I personally believe we are closer to the end point than the start point. As John Maynard Keynes supposedly noted, the market can remain irrational longer than we can remain solvent.

Now, a very quick history lesson on events that happened 45 or so years ago and why this has created numerous property bubbles in Australia and the world. In 1968 then US President Lyndon Johnson eliminated US dollar gold cover. That is, the US no longer had to have a percentage of gold in their reserves to cover each US dollar that was in existence. This was taken a step further in 1971 by the then US president Richard Nixon who suspended the US dollar’s convertibility into gold, which meant that a US dollar could no longer be exchanged for gold.

Prior to this, under the Bretton Woods agreement in 1944, the US dollar was backed by gold and by proxy, so were the world’s currencies as they were valued against the US dollar on the exchange rates.

When the gold link was severed, the world changed from a gold backed to a credit backed and driven economy. This meant the economy would only grow if credit was increasing, so people were greatly encouraged to accumulate more debt by governments and central bankers. Many people were happy to oblige.

Anybody who bought property in the past 45 or so years has been the beneficiary of this huge loosening of credit brought about by the actions of both Presidents Johnson and Nixon.

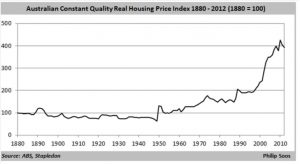

When looking at Australian house prices from about 1880 until late 1960’s/early 1970’s, prices were relatively flat, when adjusted for inflation. Once credit was loosened however, from the late 1960’s onward house prices went parabolic over and above the inflation rate. The gains seen over the past 45 or so years are a product of this huge credit expansion.

Pretty much anybody who purchased property in that time, benefitted from increasing values. With few exceptions, property prices generally went up far in excess of the inflation rate.

The people who benefitted from this windfall weren’t geniuses, they were just in the right place at the right time. But many thought they were, because they made money each time they sold property and because they didn’t understand the underlying parameters that allowed this to occur.

So the myth of property prices doubling every seven to 10 years was born. The fact that this had only happened over the past 45 or so years wasn’t recognised. “45 years” somehow became “always”.

There were even pretty graphs with a starting year point and an ending year point to support this property doubling “fact”, but once again, the data was extrapolated and prices averaged out over the time frame, rather than show actual annual prices for the period in question. And more often than not, these were not adjusted for inflation. As previously mentioned, inflation adjusted property prices stayed fairly flat until the late 1960’s. They certainly didn’t double, for example, from 1910 to 1920 or 1930 to 1940, but the graphs made it appear as though it did.

However, in the current environment of low inflation and low interest rates, property prices are now starting to pull back and I believe they are reverting back to the more normal mean of only increasing in line with inflation.

Changing demographics as baby boomers retire and change from spenders into savers, will impact on property prices as well, particularly when they start to sell their assets to fund their retirement. Not just prices for property, but shares and businesses as well.

Overbuilding of flats around Australia’s capital cities will also have a dampening effect on housing prices, particularly in attached dwellings. Real sustained property price corrections could happen as soon as the 2017-2018 financial year, if not sooner.

The way global economies are at the moment, there are no guarantees that prices will remain stable, let alone increase any time soon. And with the oversupply of flats coming into the market, most likely just as the global markets enter a serious downturn, falling real estate prices are a very real possibility, particularly from investors exiting the market. When they are not seeing any real capital gain (after inflation), have very low or no yields and longer vacancy periods, but still have to put their hand in their pocket every month for expenses, there could be a rush for the exits.

Real estate, after all, is a non-productive consumption item.

Prices may rise but people seem oblivious to the fact they can also fall. What goes up can also come down. So capital gain only really exists if it is realised. Unless capital gain is locked in (ie. sold at the highest valuation price), it’s not real capital gain. You cannot rely on the greater fool theory forever. This is the theory that a greater fool will come along and pay you more for your “asset” than you paid for it initially. The banks have been complicit in this, allowing borrowing against any increase in equity so the debt load is constantly increasing. This strategy is also pushed by property spruikers as a means of increasing your property portfolio.

Yes, a property investor might have a two million dollar property portfolio. But if it’s secured against a debt of $2.5 million thanks to falling property prices, that’s hardly a sound financial position to be in. If and when that happens, the friendly bank won’t be quite so friendly any more.

The problem is that, as previously mentioned, housing is a non-productive consumption item whose purpose is to provide shelter, but is being sold as an investment item reliant on capital gain to create wealth rather than yield to provide cash flow.

So, as well as property not doubling every seven to 10 years over a long period of time, Australian property prices can also actually fall. And this is even more likely at this particular juncture.

We are entering a deflationary period, a period of asset price falls. The reason the massive money printing or quantitative easing programs we have seen over the past few years by many countries have not succeeded in increasing asset prices consistently, kick starting the economy or causing massive inflation or even hyperinflation, is that this money printing has just stopped the deflationary forces from having their full effect. It’s why the global economy is sluggish at best. With the amount of money printing carried out by various governments, global economies should be booming. They are not.

Just as record low, and in some cases negative, interest rates have similarly been unsuccessful in getting the global economy moving.

There is a train of thought, particularly amongst politicians and central bankers that inflation is good and deflation is bad. But I disagree. Before the turn of the last century, (and incidentally before the proliferation of central banks), deflation was as much a part of an economy as inflation. Before the 1900’s, periods of inflation were generally always matched with periods of deflation.

It was only when central banks decided that deflation was a bad thing that we have had persistent inflation. Inflation has only been a feature of modern economies from about the early 1900’s onwards (incidentally, the US Federal Reserve Bank came into being in 1913).

Why is deflation the enemy? Deflationary periods are useful to dampen and remove mal-investments from the markets and bring the economy back into equilibrium. This is now being prevented from happening.

Japan is well into its third decade of deflation. Asset prices (property, stocks and businesses) are about half the value they were during the 1980’s and have never recovered those highs. The various governments of the day have tried desperately to stimulate inflation and asset price growth through massive quantitative easing (far greater than the US) and zero and negative interest rate policies. It hasn’t worked. Inflation is still negligible and asset prices are still languishing. And yet Japan is still ticking along nicely and they’re in no immediate economic trouble. Why? Because inflation isn’t needed!

And why are our politicians and central banks so desperate to see inflation? Because it increases asset prices, which brings about the so called “wealth effect”. When asset prices are rising, people feel wealthier and more secure and this supposedly encourages people to spend more. And why is this a good thing? Because under a fiat (debt backed, not gold backed) monetary system (pretty much all developed nations and most developing nations) in order for the economy to grow, we need to borrow more and get further and further into debt. In other words consume today with tomorrow’s income.

The record amount of debt we currently have in Australia does not bode well either. Australia is currently one of the most indebted nations in the world. We have record amounts of private and corporate debt, and public debt is increasing faster than any other developed nation.

Rising public debt endangers our AAA credit rating, which in turn will increase borrowing costs for the major banks causing interest rate rises above the RBA “official” rate. Many of the private debt holders won’t be able to afford any interest rate rises. A massive amount of this private debt is secured against this non-productive consumption item, property, which will either be defaulted upon or sold at a loss.

What does this mean for the housing bubble? Who knows! It could continue for another 10 years, start to deflate next month or pop in a year.

The markets can only be gamed for so long before they revert back to the mean. We are probably now entering an extended deflationary period and sluggish global economic growth, after more than 100 years of constant inflation. Get used to it. This is most likely the new normal.

![]()